August 2024 Residential Market Update Highlights for the Kansas City Region

August 2024 is going to be know as the month that real estate changed with the new NAR and MLS rules starting in the KC area on August 14. How did that impact the market? In my opinion, not all that much.

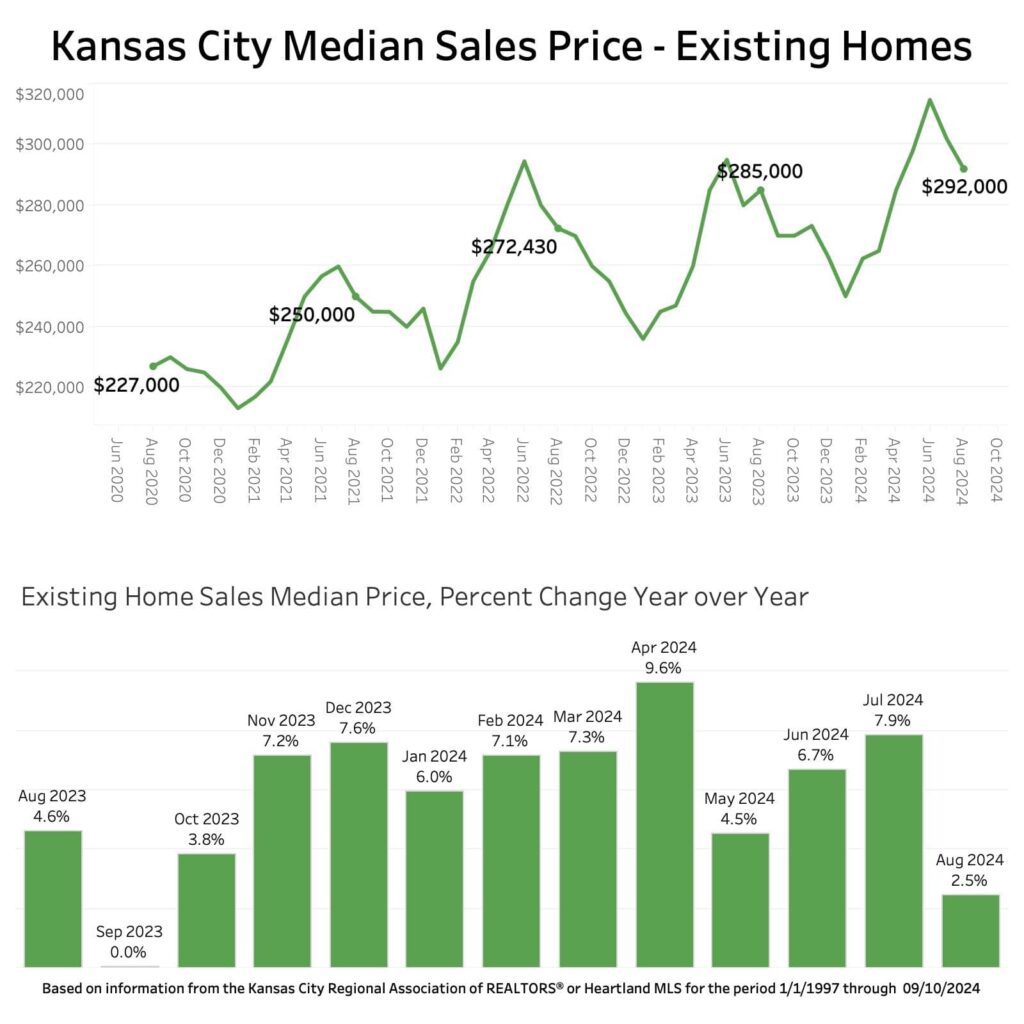

Starting with the median sales price for existing single-family properties we still saw a small increase of 2.5% over August 2023.

Looking forward we should expect another decent increase for September but after that we start to get into a string of 11 straight months where the increase is over 6% every month making it harder to see these increases every month since the previous year saw large increases.

We are also seeing the monthly median price drop from the previous month’s median. Still again this is to be expected as the Kansas City area usually sees the highest median sales price in June every year and then small decreases each month until February of the next year but maintaining the monthly year-over-year growth.

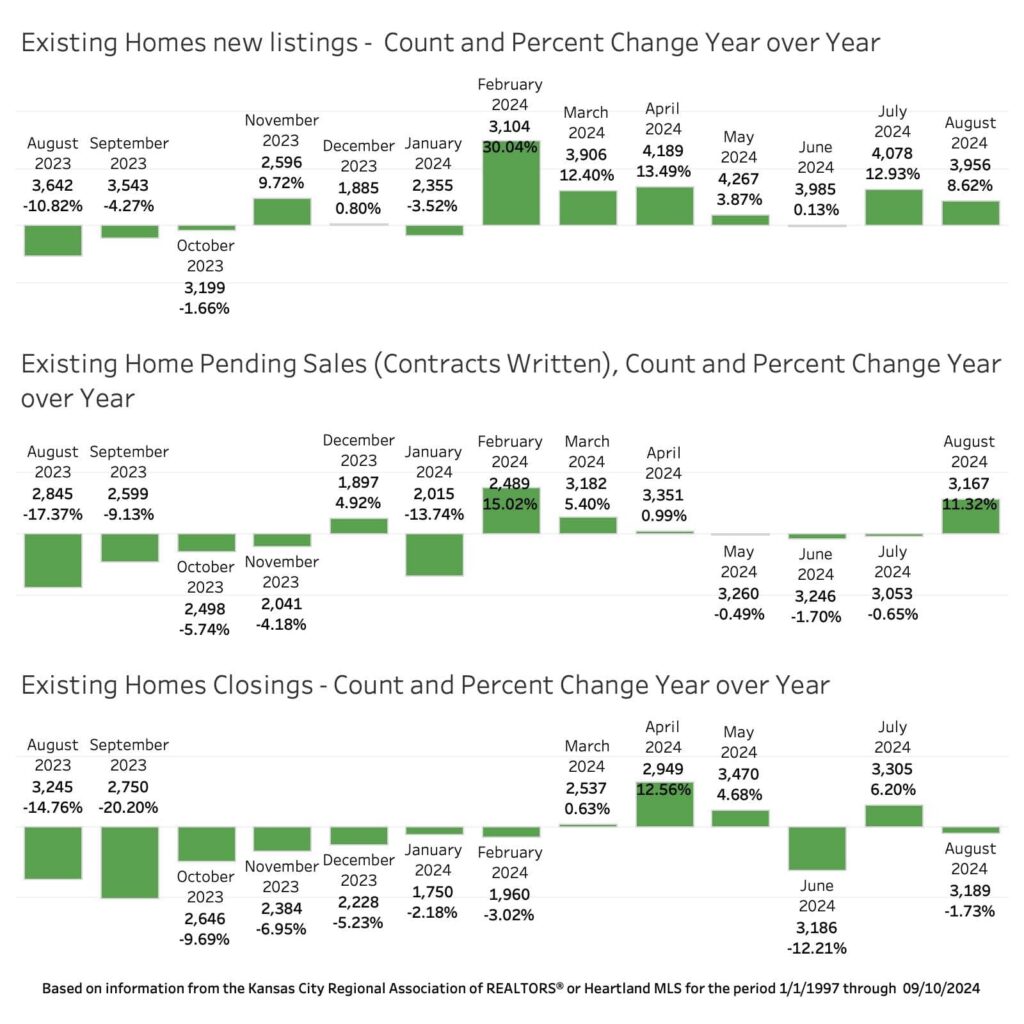

New listings continued a solid growth with an 8.6% increase over August 2023 following an almost 13% increase in July. As interest rates continue to fall (6.22% as of today according to Mortgage News Daily) the low interest rate lock in for sellers is not quite an impediment to selling as it was when interest rates were approaching 8% earlier this year. Every month since February has shown an increase in homes hitting the market.

The July and August increase in listings lead to a large increase in contracts written with an 11.3% increase. My thought is interest rates impact the number of contracts written but the number of homes for sale have just as much if not more of an impact as we saw a similar jump in contracts written in February when we had a 30% increase in new listings and saw a 15% increase in contracts written. This increase follows three months of negative growth in contracts written.

The increase in contracts written didn’t show up yet in the closings but like February’s large increase in contracts written didn’t show in the closings until April we can expect to see an increase in closings in September and October.

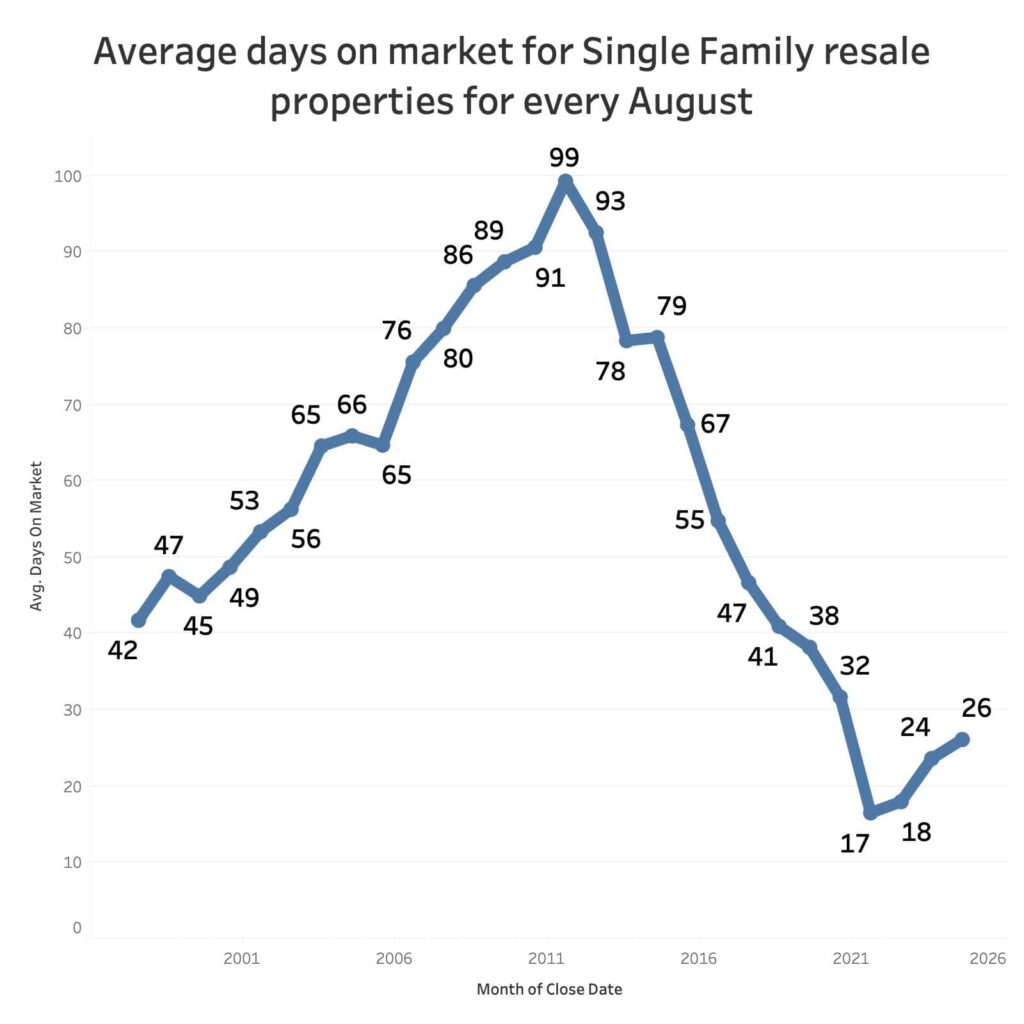

Days on market continue there slow rise to 26 days after reaching an August low of 17 days in 2021. This is still less than 1/3 of the August high of 99 days on the market in 2011 and still half of August 2001 at 53 days.

Headwinds for the market are starting to go away after the NAR changes in August and lower interest rates but it is an election year. Both parties have given ideas at what they would like to do to increase affordable housing. The focus needs to be on the supply side and increasing the number of new single family homes being built that address the missing middle and attainable housing. As we saw with the covid stimulus funds, giving large amounts of money to the demand side increased the cost of housing and increased inflation due to housings large impact on the economy.

If you want to dive deeper into these numbers, visit Kyle’s Website at https://www.housegraphs.com/marei or join him at the next WinVestor’s meeting.

Catch up on past data