If you only follow headlines, it’s easy to think the housing market is either perfectly fine or on the brink of collapse.

The truth — as usual — is more nuanced.

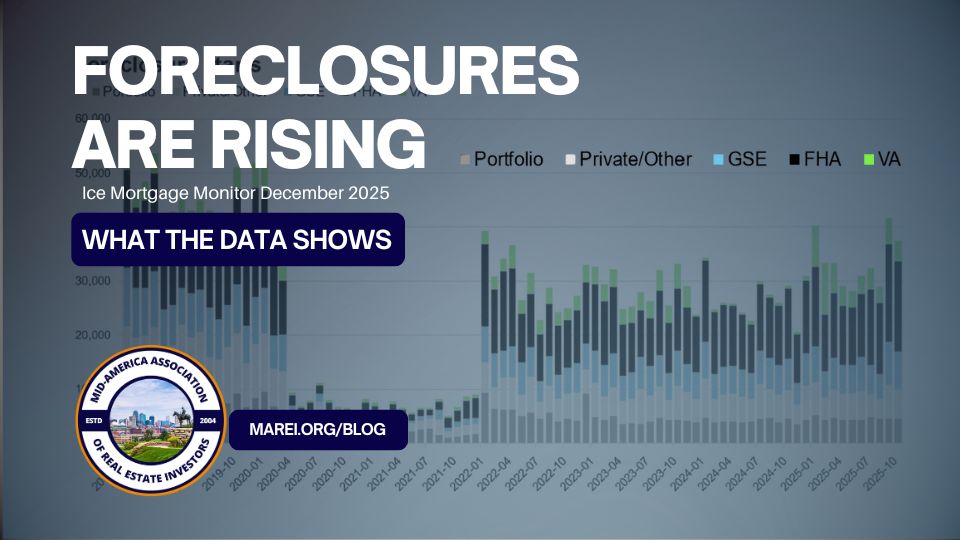

Foreclosures Are Quietly Rising — Here’s What the Data Shows and Why Short Sales Matter Again

The most recent ICE Mortgage Monitor Report shows that foreclosure activity is increasing, but not evenly across the market. Overall mortgage performance remains relatively stable, yet a specific segment of borrowers is beginning to show real stress. That stress is now showing up clearly in foreclosure starts and active foreclosure inventory.

This is not a replay of 2008.

But it is a shift — and for real estate investors, understanding where that shift is happening matters.

What the Foreclosure Data Is Actually Showing

According to ICE, foreclosure starts and active foreclosure inventory are up meaningfully year-over-year, even as overall delinquency rates remain below pre-pandemic levels. In other words, this is not a broad-based consumer credit collapse.

Instead, the data points to concentrated distress.

Foreclosures are rising:

Selectively, not universally

Gradually, not explosively

And disproportionately within certain loan products

One category stands out consistently in the data: FHA loans.

Where the Stress Is Concentrated: FHA Loans

FHA loans were designed to expand access to homeownership, and they’ve done exactly that. But the same features that make FHA loans accessible also make them more vulnerable when market conditions change.

Many FHA borrowers entered homeownership with:

-

Low down payments

-

High loan-to-value ratios

-

Limited equity buffers in the early years

That structure works well when prices are rising quickly. It works far less well when appreciation slows or stalls.

In fact, 1 out of every 10 FHA loans in America is currently delinquent according to the Mortgage Bankers Association.

The ICE data shows FHA loans making up a growing share of:

-

Serious delinquencies

-

Foreclosure starts

-

Active foreclosure inventory

-

With the average loan being 632 days late.

This isn’t about borrower quality. It’s about math.

Why the Usual Exits No Longer Work

For years, homeowners who ran into trouble often escaped without ever entering foreclosure. Appreciation covered mistakes. Refinancing reset the clock. Selling solved the problem.

That dynamic has changed.

Low Interest Rates Don’t Equal Liquidity

Many FHA borrowers have interest rates in the 2–3% range. On paper, that sounds like a safety net.

In practice, it often isn’t.

If a homeowner still owes 95–97% of peak market value — which is common for FHA borrowers who bought in 2021–2022 — a traditional sale becomes difficult once you factor in:

Realtor commissions

Closing costs

Repairs or deferred maintenance

Even with a low rate, the homeowner may not be able to sell and fully satisfy the loan.

Refinancing Isn’t a Reset Button Anymore

Higher rates and tighter underwriting standards have removed refinancing as a reliable exit. Many borrowers simply don’t qualify, and even those who do often face higher payments.

Without appreciation or refinancing, pressure builds.

The Quiet Wind-Down of FHA Loss Mitigation

Foreclosures did not immediately spike after the pandemic for a reason.

FHA loss-mitigation programs — including forbearance, deferrals, and loan modifications — played a major role in delaying foreclosure activity. These programs worked best when:

Incomes rebounded quickly

Home values continued to rise

Borrowers could eventually refinance or sell

Today, many of those pandemic-era protections have either expired or reached their practical limits.

Loan modifications can:

Extend terms

Capitalize arrears

Reduce payments

But they do not solve principal imbalance. When income doesn’t stabilize or equity remains thin, loss mitigation delays the outcome — it doesn’t prevent it.

The ICE data now reflects this reality: a growing share of seriously delinquent FHA loans are transitioning into foreclosure rather than curing.

Why Subject-To Breaks Down in These Situations

Over the past several years, Subject-To became the default solution for distressed properties with low interest rates. In the right conditions, it worked.

Those conditions are no longer the norm — especially for FHA loans.

FHA Loans Change the Rules

FHA loans are federally insured and governed by stricter compliance standards. Unlike many conventional loans, FHA loans do not allow ownership transfers without lender approval.

When a property is purchased Subject-To:

Title changes

Insurance changes

Tax records change

FHA servicers are far more likely to flag these transfers. When that happens, the loan can be accelerated and called due — even if payments are being made.

This isn’t theoretical. Investors are seeing it happen.

Thin Equity Makes Subject-To Risky

Subject-To works best when there is:

Strong equity

A performing loan

Time to stabilize the property

Many FHA foreclosure cases today involve:

Missed payments

Arrears that must be cured

Deferred maintenance

Minimal or no equity

At that point, the low interest rate doesn’t offset the risk.

Why Short Sales Fit This Market Shift

Short sales exist for a reason — and the current data highlights that reason clearly.

Short sales are designed for:

-

Non-performing loans

-

Active lender involvement

-

Borrowers who cannot sell traditionally

-

Situations where time and negotiation matter more than speed

A properly structured short sale:

-

Eliminates arrears

-

Resets the basis

-

Removes due-on-sale risk

-

Transfers clean title with lender approval

- Pays the borrower some money at closing

In FHA distress situations, this matters.

Short sales don’t rely on workarounds. They resolve the loan according to lender rules.

What This Means for Real Estate Investors

This isn’t a foreclosure wave driven by volume.

It’s a process-driven opportunity window.

The data suggests we are entering a phase where:

Distress appears earlier than listings

Many properties sit in foreclosure limbo

Negotiation matters more than leverage

Process beats speed

Investors who understand lender timelines, borrower motivations, and documentation requirements are positioned very differently than those relying on strategies that assume clean, performing loans.

As foreclosure data shifts, short sales are back in the conversation for real estate investors.

That’s why February at MAREI is focused on short sales, with multiple chances to learn from David Randolph, a specialist who’s been navigating short sales since the last major downturn.

Upcoming February Events:

-

MAREI Meeting – Feb 10

-

WinVestors – Feb 11

-

Virtual Master Class – Feb 28

📅 Full details available on the MAREI Calendar

The Bottom Line

The foreclosure data does not point to a housing crash.

It does point to stress forming in specific, identifiable places — particularly within FHA loans where thin equity, expired loss-mitigation tools, and limited exit options collide.

For investors, foreclosure data isn’t about fear.

It’s about understanding where opportunity forms before it becomes obvious.

Source:

ICE Mortgage Monitor Report (December 2025)

Market Update